Editors’ Note:

Hi, it’s Laura and Jonathan again. As a reminder, we’re taking the wheel here every other edition and Tim will be back with you in a couple weeks. One question kept surfacing as we assembled this edition. Emergency savings advice built for stable households, child savings accounts that work best for families who already have 529s, and jobs policy that still imagines a mid-20th century labor market—Who are these systems designed for, really?

— Laura Freschi and Jonathan Morduch

1. The $1,000 question

Laura: A lot of personal finance advice is built on a quiet assumption: that the person taking the advice has a baseline level of financial stability. Save three to six months of income, the financial gurus intone, as if the main problem is discipline rather than the fact that for a large share of American households—whether they’re in gig work, earning hourly wages, or heading up a struggling small business—income is volatile, expenses are unpredictable, and a single bad month can wipe out whatever cushion they had. The advice isn't wrong; it just describes a world that a lot of people don't live in.

What would actually help? Rachel Schneider, the founder and CEO of the non-profit Canary, who not coincidentally co-authored the US Financial Diaries with Jonathan, offers one answer. As she explained on Marketplace, Canary helps employers fund emergency grants when employees hit a crisis. The interview calls it “palliative care," which sounds superficial until you consider that for a lot of households, a “usefully large lump sum” of $1,000 is exactly what is needed at that moment.

There is research (not just our own) to back up this idea. The Aspen Institute found that $1,000 in emergency savings cut in half the likelihood of workers raiding their retirement accounts during the pandemic. And the JPMorgan Chase Institute found that $1,000 in cash savings is enough to reduce financial distress: households relying on a plan to cut discretionary spending when an emergency hits miss nearly three times as many payments as those with cash on hand.

2. Saving young

Laura: In our hyper-politicized environment it’s not a stretch to think that a large number of Americans hear about a thing called “Trump Accounts” and immediately put them in the same mental bin as Trump Steaks or Trump Coin.

And yet, the core idea behind the Trump Accounts—tax-advantaged savings accounts for children—has a long, respectable, and bipartisan history (listen to this episode of the podcast Optimist Economy for the deep dive). Michael Sherraden, an economist at WashU, argued 35 years ago in his book “Assets and the Poor” that we needed a way for all kids—not just those born to parents who already own homes and 401Ks—to build assets, starting from birth. Since then, lawmakers in many states and a few other countries have taken the idea to build programs like Connecticut’s Baby Bonds, and Oklahoma’s SEED OK Account.

Created as part of last year’s “One Big Beautiful Bill” Act and set to go live this July 4th with a government contribution of $1000 for all kids born between 2025 and 2028, the Trump Accounts could bring Sherraden’s idea to millions more children. Sherraden himself, with co-author Ray Boshara, wrote an op-ed supporting the policy, with a few suggestions for improvement. There are plenty of ways to make the Trump Accounts more inclusive, and more pro-poor. Making enrollment automatic upon birth, rather than asking parents to opt in, is the first. A regulator paying attention so that investments are not targets for predators (either during childhood or as soon as the accounts can be drawn on). Not funneling the whole process through the tax system, since 10% of kids live in families that don’t file taxes. Offering larger deposits to kids from poorer families since, let’s face it, rich families already have plenty of ways to save. And changing the name to something less divisive…also couldn’t hurt.

3. Jobs

Jonathan: Earlier in the year, experts were asked by NOTUS: “Which issue, trend or crisis will dominate global economic news in the year ahead?” If asked today, the answer surely would be the intensifying US war with Iran. Before the war, one answer was “jobs”.

Ayhan Ghose, deputy chief economist of the World Bank, started with this challenge: “By 2035, about 1.2 billion young people will reach working age in the developing world, flooding labor markets that are already struggling to keep pace.” About 40% of those young people live in “fragile and conflict-affected settings.” Without jobs, unemployment will spike, and widespread unemployment increases the risk of political crises. Ghose argues that the old playbooks for job creation are unlikely to work in the present and future. But his prescriptions in fact sound a lot like the old World Bank playbook: mobilize private capital at scale, invest in human capital, ensure macro policy is stable, create “enabling” business environments...

One thing Ghose doesn’t stress is that the looming jobs crisis will likely hugely expand informal jobs, which offer few protections and where workers are forced to shoulder risks that are better absorbed by their employers. Laura Alfers of WIEGO, an organization that focuses on women and the informal economy, offers a more interesting start. If we want to take jobs seriously, says Alfers, we need to recognize “a slow-burning tension that has been building for years”— the gap between the realities of life in the informal sector, contingent and unsteady, and how the state approaches work and regulation as if we still lived in “a mid-20th-century model of stable, full-time employment.” That actually sounds like the start of a new playbook.

4. Love letters

Jonathan: Here at FAI, we’re particularly interested in the digitization of modern life—especially digital money. So the love letter to love letters—the kind with stamps and envelopes that you lick to seal—from the Danish writer Anna Juul caught my attention. As of December 30, 2025, mail as we used to know it—faithfully delivered through rain and sleet and gloom of night—is no more in Denmark. Now it’s email and SMS and WhatsApp all the way down. “It reminds me that I live in a country that would be completely and utterly f***ed if there was a power cut or an internet outage,” says Juul. But then: “Maybe I would have been less lonely if I’d had an online community instead of a crappy penpal. Either way, the old world isn’t coming back. Unless you go to Germany, of course.”

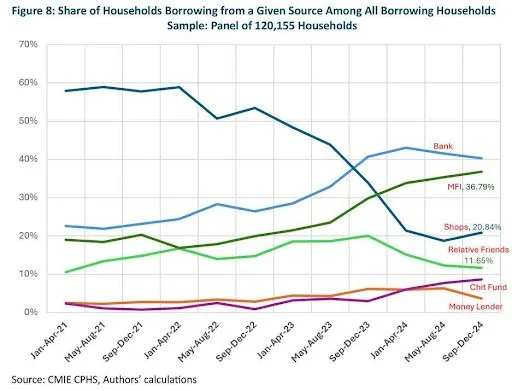

5. Microfinance rising

Jonathan: You might think that microfinance is so over, just like Danish love letters. But while we’ve been chewing over the RCT results on microfinance impacts, the latest data shows that microfinance is in fact very much alive in India—and steadily growing. This chart from recent research by a team at Dvara Research in Chennai shows microfinance ascendent.

The data are from the Consumer Pyramids Household Survey, a private-sector initiative, which has plenty of problems beyond just its name. Still, the rising share of microfinance institutions (MFIs) in overall lending, from 10% in 2021 to 37% less than three years later, is striking, especially if the evidence is confirmed in other data. Dvara is not celebrating, though: along with microfinance has come a troubling rise in “debt distress.” A question is whether consumer protections will be strong enough in practice to limit the negative consequences of increased debt while allowing others to be helped by greater access to capital.

The data are from the Consumer Pyramids Household Survey, a private-sector initiative, which has plenty of problems beyond just its name. Still, the rising share of microfinance institutions (MFIs) in overall lending, from 10% in 2021 to 37% less than three years later, is striking, especially if the evidence is confirmed in other data. Dvara is not celebrating, though: along with microfinance has come a troubling rise in “debt distress.” A question is whether consumer protections will be strong enough in practice to limit the negative consequences of increased debt while allowing others to be helped by greater access to capital.

The faiV is written by Timothy Ogden, Jonathan Morduch, and Laura Freschi, and produced by the Financial Access Initiative at NYU's Wagner Graduate School of Public Service.

Email: fai-wagner@nyu.edu

To read this in your inbox, subscribe to the faiV.